Danger administration is an important side of investing, and lots of buyers search instruments to guard their portfolios from market volatility. Amongst these instruments, the VIX index, also called the concern index, holds a outstanding place. As a measure of the implied volatility of choices on the S&P 500 index, the VIX provides a novel technique to hedge towards market fluctuations. This text explores the position of the VIX in portfolio hedging and the way buyers can use it to scale back dangers related to market volatility.

What’s the VIX?

The VIX (Volatility Index), typically known as the “concern index,” is an index that measures the anticipated volatility of the US inventory market, particularly the S&P 500 index, over a 30-day interval. It’s calculated utilizing the costs of choices on the S&P 500 index and represents implied volatility, that’s, the variation anticipated by buyers available in the market. A excessive VIX signifies that buyers anticipate excessive volatility, which might sign elevated uncertainty, typically linked to macroeconomic or geopolitical occasions. Conversely, a low VIX displays a perceived interval of stability within the monetary markets. Thus, the VIX is a barometer of concern and confidence within the markets.

Why use the VIX to hedge a portfolio?

Funding portfolios are naturally uncovered to volatility dangers, which might result in substantial losses, particularly in periods of financial or geopolitical uncertainty. The VIX permits buyers to guard themselves towards this elevated volatility and scale back the unfavorable influence of market fluctuations. Listed below are some explanation why the VIX is a worthwhile software in portfolio hedging:

Hedge towards market declines: In periods of excessive volatility, shares can expertise important worth drops. The VIX, as a measure of volatility, typically rises throughout market declines. Consequently, by holding derivatives based mostly on the VIX, reminiscent of futures or choices, buyers can revenue from the rise within the VIX in periods of disaster.

Safety towards unexpected occasions: The VIX is especially helpful for shielding towards unexpected occasions that may set off sudden and important volatility within the markets, reminiscent of a monetary disaster, struggle, pandemic, or main political selections. Throughout such occasions, the market typically reacts excessively, resulting in a pointy enhance in volatility, which is mirrored in an increase within the VIX.

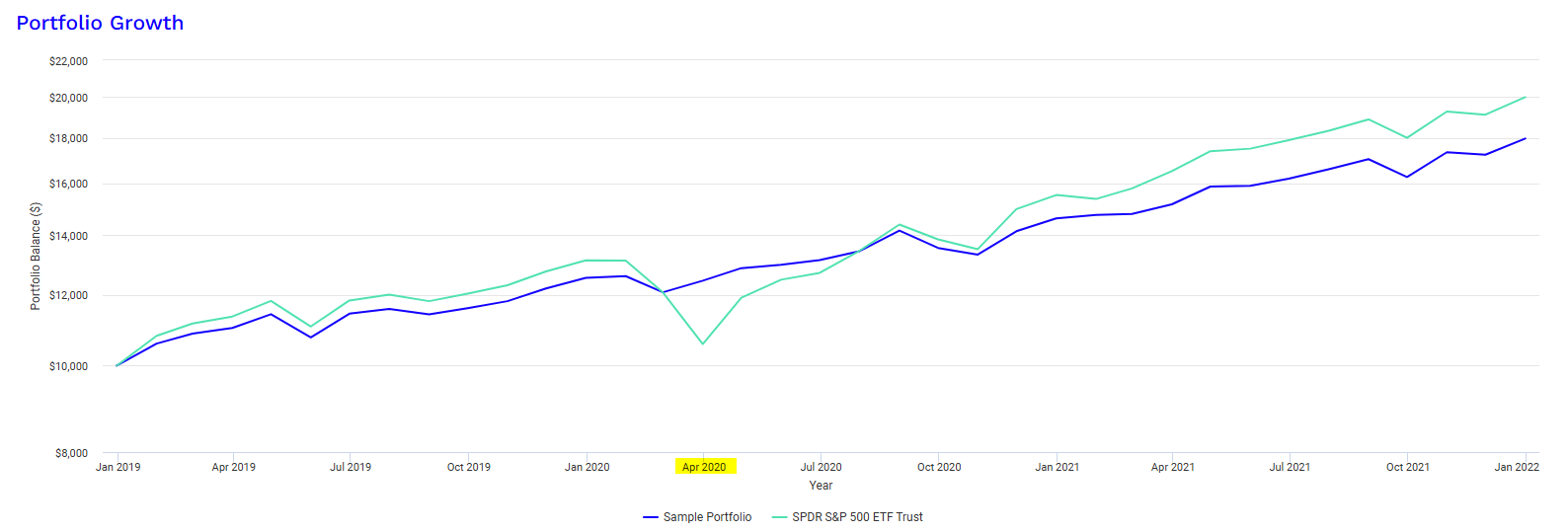

Decreasing publicity to market declines whereas sustaining upside potential: The VIX will also be used to scale back publicity to declines whereas sustaining some upside potential. A diversified portfolio that features shares, bonds, and different belongings may be susceptible to volatility. Reasonably than promoting shares or considerably decreasing fairness positions to restrict danger, an investor can purchase choices on the VIX for hedging.For instance, right here an allocation with 5% UVXY and 95% SPY averted a drawdown through the covid disaster in March 2020:

Volatility of volatility: dynamic danger administration: One other essential characteristic of the VIX is that it provides dynamic danger administration. In contrast to extra static hedges, utilizing the VIX permits buyers to react shortly to altering market circumstances. The VIX is a very versatile software as it may be used based mostly on the anticipated route of the market (rising or falling volatility) and the specified depth of the hedge.

Tips on how to use the VIX to hedge a portfolio?

There are a number of methods for buyers to make use of the VIX in hedging their portfolios. The principle strategies embrace:

VIX futures contractsOn Etoro you could have entry on two VIX future contracts entrance months:

VIX choices

VIX-based ETFs and ETNs

Listed below are some ETFs and ETNs on Vix that you could find on Etoro:

Limitations and Dangers of Utilizing the VIX

The Dangers Related to Utilizing VIX Futures and ETNs: The Rolling Price

The VIX index, typically dubbed the “concern index,” measures the implied volatility of choices on the S&P 500 index over a 30-day interval. Whereas it’s a worthwhile software for hedging towards market fluctuations, utilizing VIX futures and exchange-traded notes (ETNs) carries important dangers. One main danger is the rolling price, a phenomenon that may negatively influence long-term returns.

Understanding Rolling Price Rolling price is a attribute of futures contracts, that are monetary contracts that enable buyers to guess on the longer term route of an asset’s worth (on this case, volatility). VIX futures are sometimes used to hedge towards rising volatility or to take a position on market route. Nonetheless, these contracts have a restricted period and expire after a sure interval, sometimes 30 days. To take care of a long-term place in futures, buyers should “roll” their contracts. This entails promoting expiring futures contracts and shopping for contracts with a later expiration date. Rolling price happens when short-term futures contracts (these expiring quickly) are cheaper than longer-term futures contracts (these with a extra distant expiration). When an investor buys a costlier futures contract to interchange an expiring one, they incur a loss because of the worth distinction. This phenomenon is amplified in a market state often called contango, the place longer-term futures contracts are persistently costlier than shorter-term ones. Rolling price then turns into a unfavorable issue for the long-term returns of futures and ETNs.Let’s take an instance for instance the price of roll over on VIX futures:

Let’s assume that the longer term short-term VIX is buying and selling at 14.2 and the longer term long-term VIX is buying and selling at 15.9.

If an investor holds the futures contract expiring in December and needs to proceed holding a place, he should promote his contract expiring at 14.2 and purchase a long-term contract at 15.9.

This creates a right away lack of 1.7 factors for the investor, merely because of the worth distinction between the short-term and long-term contracts.

This phenomenon can have a considerable influence on long-term returns, particularly in a market the place volatility is low, however long-term futures costs stay excessive attributable to persistent contango.

Rolling Price in VIX Futures VIX futures are by-product devices that enable buyers to take a position on future market volatility or hedge towards elevated volatility. As talked about earlier, these contracts have mounted expiration dates, and to keep up an open place, buyers should roll their contracts.

Rolling Price in VIX ETNs Alternate-Traded Notes (ETNs) linked to the VIX, such because the VXX or UVXY, are monetary merchandise that enable buyers to achieve publicity to volatility with out straight coping with futures contracts. These ETNs are sometimes utilized by buyers to achieve publicity to the VIX in a less complicated approach. Nonetheless, these merchandise are additionally affected by rolling prices. ETNs sometimes spend money on VIX futures contracts, and once they roll these contracts, they encounter the identical contango drawback as futures. Because of this, ETNs can endure from a long-term downward bias, as they need to purchase costlier futures contracts because the previous ones expire. This may result in a gradual decline within the worth of the ETNs, even when market volatility stays excessive or the VIX will increase.

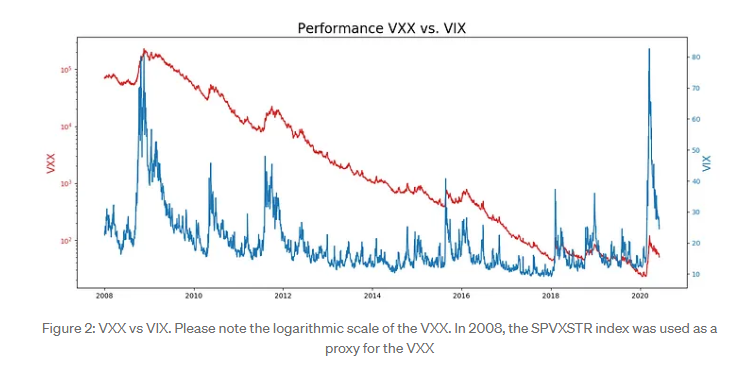

Illustration: Affect of Rolling Price on the VXX

Take into account the VXX, a preferred ETN that tracks VIX futures contracts. The chart under illustrates the influence of rolling price on this product. We examine the evolution of the VXX with that of the VIX spot (the precise worth of the VIX).

As proven within the chart, the VXX doesn’t completely monitor the VIX spot. As a result of rolling prices, the VXX reveals a downward development over the long run, even when volatility will increase. This phenomenon is attributable to contango, which drives up the costs of longer-term futures contracts, resulting in fixed losses for long-term buyers.

As proven within the chart, the VXX doesn’t completely monitor the VIX spot. As a result of rolling prices, the VXX reveals a downward development over the long run, even when volatility will increase. This phenomenon is attributable to contango, which drives up the costs of longer-term futures contracts, resulting in fixed losses for long-term buyers.The Results of Rolling Price on Lengthy-Time period Returns The consequences of rolling prices may be notably pronounced over prolonged durations. For instance, if an investor buys VIX futures or a VIX ETN just like the VXX and holds the place for a number of months or years, they may incur steady losses attributable to rolling prices, even when market volatility stays comparatively steady. The influence of rolling prices is very noticeable in periods of low volatility however excessive futures costs attributable to contango. Even when volatility will increase briefly, the impact of the worth distinction between short-term and long-term contracts can outweigh the beneficial properties realized by the investor. This phenomenon is also known as the “decay” of VIX-based ETNs.

Conclusion

The VIX is a worthwhile hedging software for buyers looking for to guard themselves towards market volatility. As a barometer of concern and uncertainty within the monetary markets, the VIX permits buyers to hedge towards market declines and unexpected occasions whereas sustaining potential upside. Nonetheless, it’s important to make use of the VIX with warning and perceive the dangers related to its use, notably in leveraged by-product merchandise. By incorporating the VIX right into a hedging technique, buyers can higher handle volatility and shield their portfolios from important losses.

{kind=link}