I’ve been investing for a big a part of my life, and I’ve by no means seen detrimental sentiment like this earlier than. Not even throughout the newest two bear markets. First for the Covid-19 crash and later when the Fed went by way of a nasty rate of interest mountaineering cycle to take care of inflation, which was for my part, self-inflicted. It ought to be famous that ”formally” each crashes didn’t include a recession, nevertheless, we do know that put up Covid the economic system shrank for the required two consecutive quarters, however there was debate over its classification as the roles market was sturdy. This can be a little gray although, since this was authorities backed, similar to actual private disposable revenue that declined in 2022 and was offset by stimulus. So, in my thoughts, the federal government shot itself within the foot to keep away from a technical recession, which created a much bigger drawback later down the road that we’re nonetheless coping with in the present day. Has a comfortable touchdown been achieved? Or are we coming in sizzling?

Bear markets by way of historical past – 56% coincided with recessionSource: Investopedia

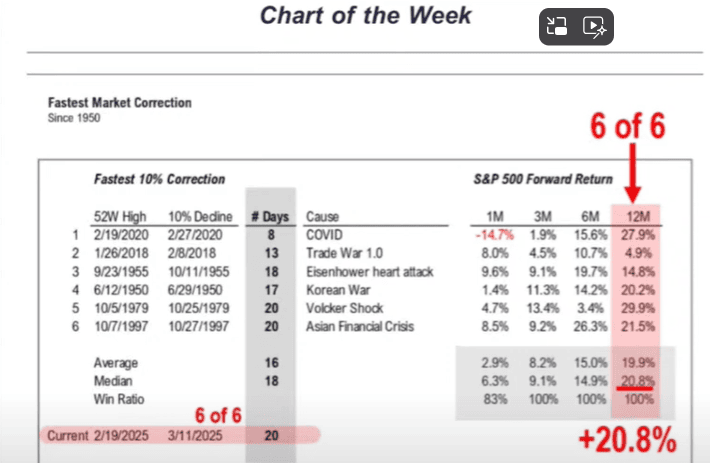

Taking a look at this current correction, the S&P 500 dropped simply over 10% in 16 buying and selling days. On common, corrections of this dimension since 1950 have taken roughly 39 days. I feel the pace of this drop is probably going what’s inflicting extra panic to construct. Different crashes that occurred at this velocity post-2000 embody the 2008 monetary disaster, debt ceiling disaster, Fed hike cycle, and COVID-19 crash. All these occasions have been a robust and speedy danger to the economic system.

What’s inflicting the drop in the present day? Tariff threats primarily, not less than that’s what the media is pushing. We have now identified for a while that this was Trump’s agenda, which begs the query why that is stunning the market a lot since they’re ahead trying. We noticed the reverse occur when he received the election and the markets pumped, excited by the concept that much less purple tape and beneficial financial insurance policies have been coming.

The truth is there are some elementary considerations, however the present market motion appears disproportionate to the underlying components, and will not totally replicate the long-term outlook.

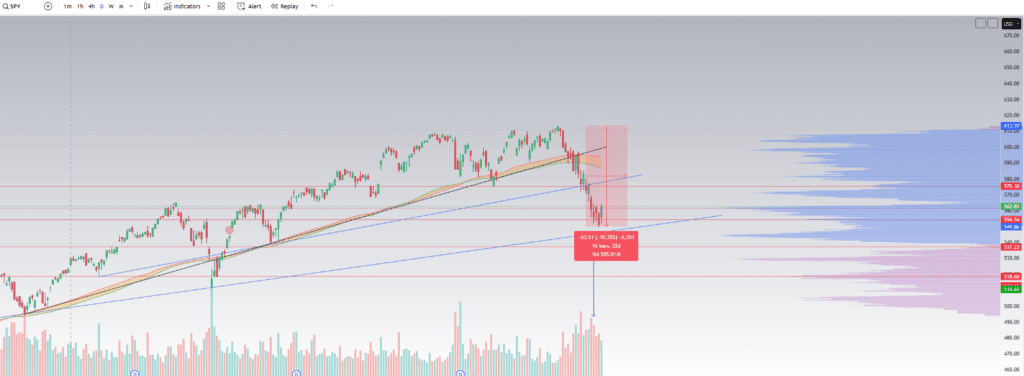

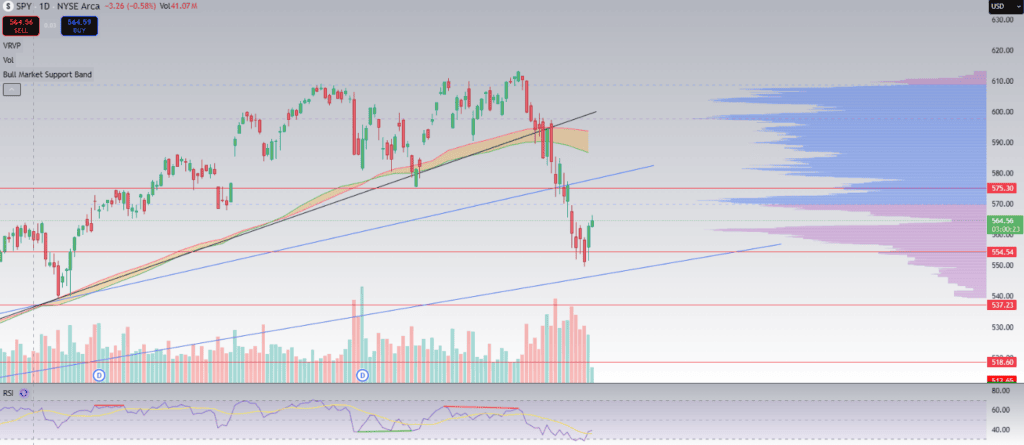

Present drop within the SPYSource: Buying and selling View chart

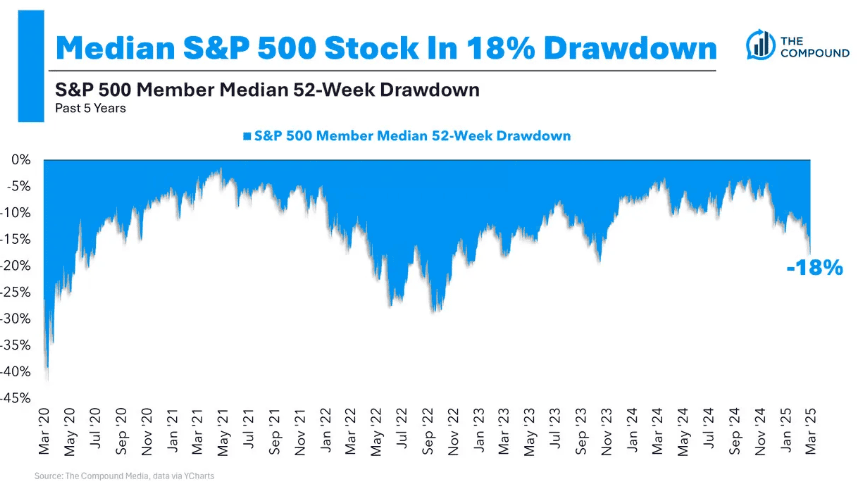

While a -10% drop doesn’t appear to be a lot; the consequence will be far more significant to shares throughout the S&P 500. Signalling some nice shopping for alternatives on some ”steady” shares.

Supply: YCharts

Sentiment

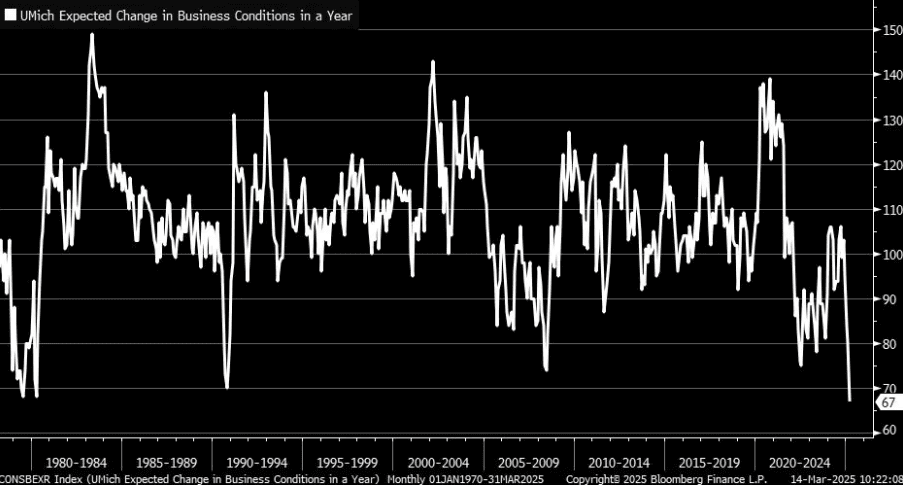

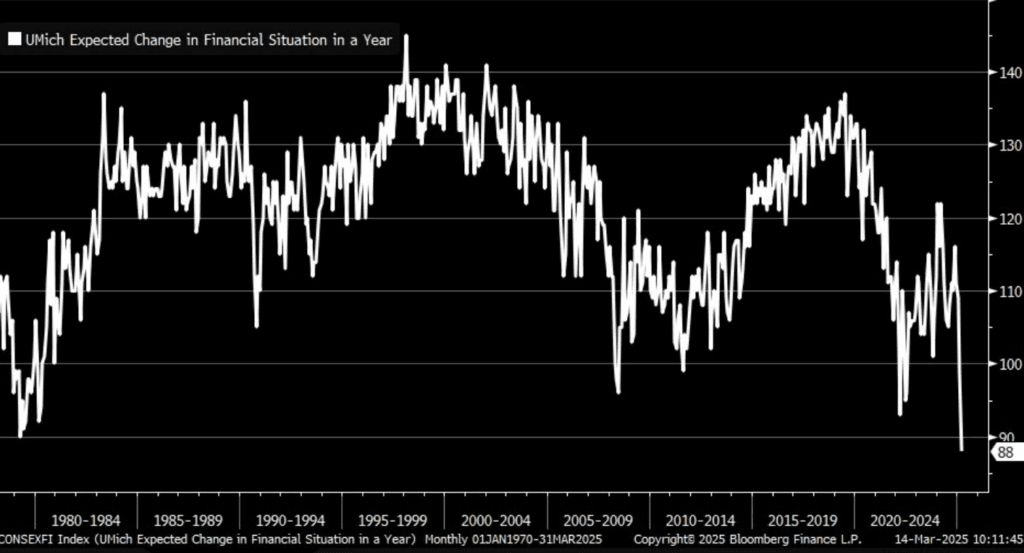

Latest knowledge has highlighted some attention-grabbing factors. Within the chart beneath we will see Michigan College’s change in enterprise situations in a yr is now essentially the most bearish it’s been in historical past. Let that sink in. The market is extra fearful than Covid, rates of interest and inflation going up. The sentiment presently displays a stage of negativity that’s unprecedented in current historical past, even surpassing the challenges seen throughout the monetary disaster and different main market occasions.

After all, take this with a pinch of salt. A majority of these surveys aren’t my favorite, and I don’t just like the teams or the way in which the info is collected, but it surely definitely strains up with a number of what we’re seeing and listening to on the market.

Supply: College of Michigan

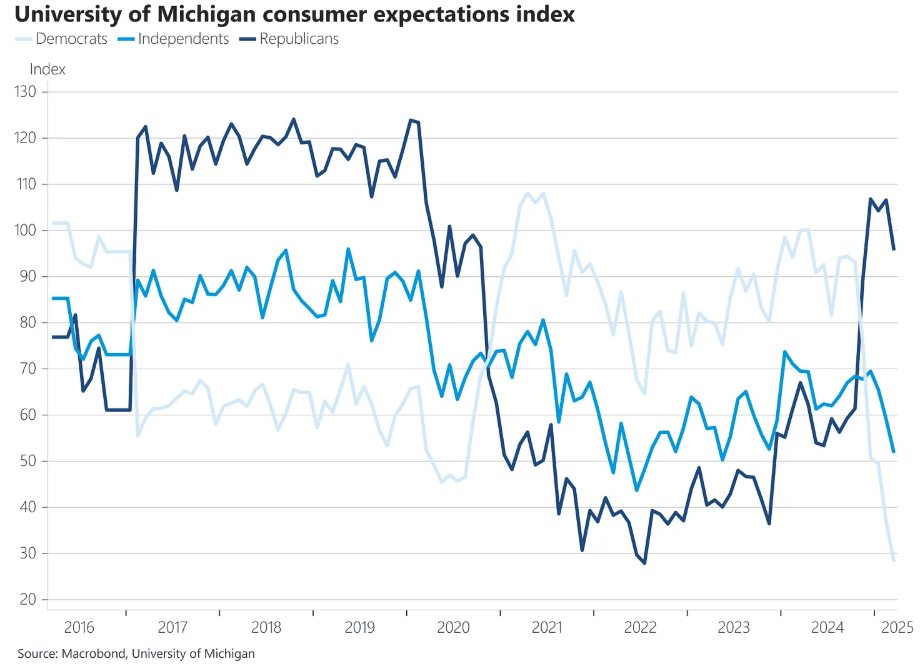

That is usually a left leaning base however even the fitting facet exhibits a detrimental outlook, simpler to determine after we have a look at their breakdown of shopper expectations between events within the chart beneath. Democrats are definitely somewhat extra… detrimental.

Supply: College of Michigan

One other chart that seems alarming at first look is the Anticipated change in monetary scenario in a yr, however paradoxically this stage of worry (Under 100) throughout earlier financial downturns has usually been indicative of the market being near its backside. We will overlay that knowledge onto the SPY and discover that in 1979, 1980, 2008, and 2022, the markets have been near peak worry and moved larger quickly after.

Supply: College of Michigan

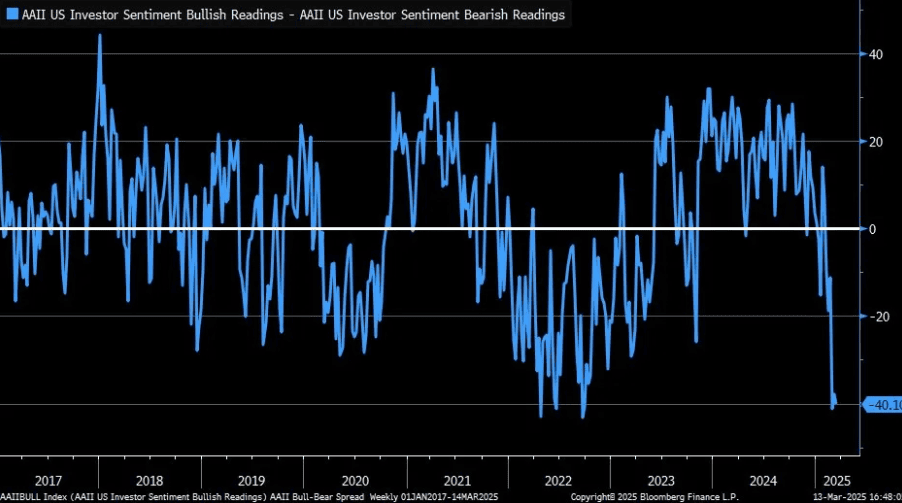

Different market sentiment gauges embody the AAII bull-bear spreads, which has fallen off a cliff. Beforehand when this stage was hit in 2022, the market recovered a couple of weeks after. I discover this one essentially the most helpful when measuring perceived sentiment. For me, it’s indicator of when is an effective time to lean into the worry, supplied that the underlying fundamentals are nonetheless on monitor after all. Scaling into positions when this metric drops beneath 20 and scaling out of positions when it’s over 20 is danger administration that is smart to me.

Supply: Bloomberg

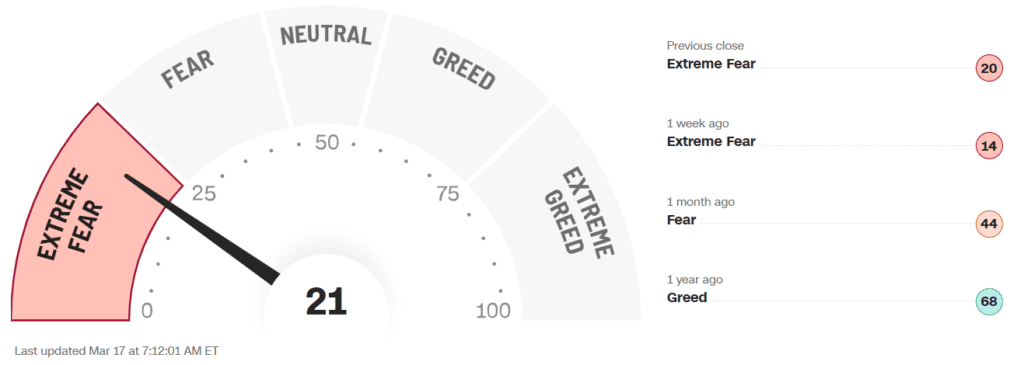

In case you would favor a extra simplistic metric to observe, the worry and greed index presents a much less correct mannequin. Lots of people wish to quote Buffet ”Be fearful when others are grasping and grasping when others are fearful.” when referring to this one and It’s going to offer you very broad strokes but it surely’s not a foul place to start out.

Supply: CNN

We additionally not too long ago acquired the New York Fed survey knowledge and yow will discover that by clicking right here. To save lots of you from extra charts I’ll follow supplying you with the cliff notes model of the info. The outcomes present a transparent acceleration in perceived danger of upper unemployment throughout most areas and demographics, with individuals additionally extra detrimental about future family funds. Placing ranges for every of those measurements again at late 2022 ranges.

The information offered aligns with established market cycles and presents insights into investor psychology, which could be a vital affect on market habits. Sentiment is usually extra necessary than the underlying knowledge and the way buyers understand that knowledge can transfer the market its methods. Headline knowledge creates sharp preliminary reactions, however wise heads take time to type by way of the noise to decide. The market on the whole will catch as much as its mistake sooner or later when information is digested and sentiment modifications. This is applicable to the broad market indexes and particular firms.

Supply: Understanding financial, market and tremendous cycles | FundCalibre

You’ll find charts and knowledge factors like this in all places with little or no effort and the explanation I’m displaying you all this knowledge is solely to indicate you that perceived danger is off the charts. Primarily based solely on these charts, one may conclude that there are vital dangers forward. Nonetheless, it’s important to think about a wider vary of financial indicators earlier than drawing conclusions.

What triggered the dangerous sentiment?

The brand new huge dangerous fear we should take care of is recession. Economists have been yapping about it for an age, and so they couldn’t have been extra improper over the previous few years. Might this be considerably impacted by their reluctance to name the put up Covid financial contraction a recession? Perhaps.

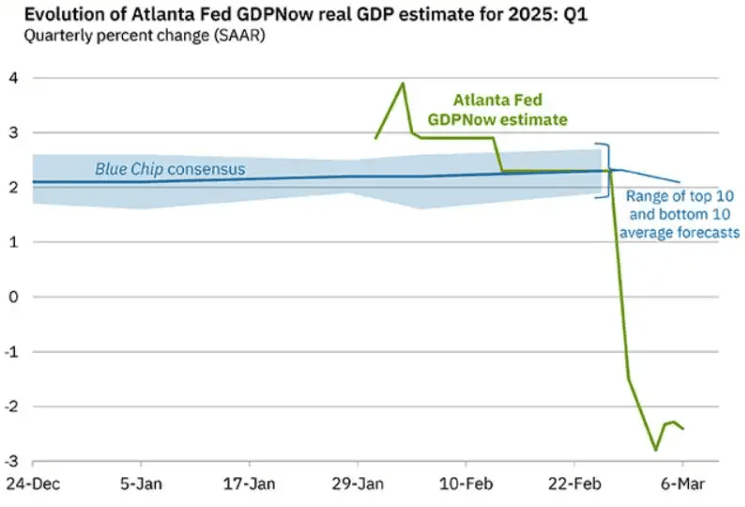

Considerations over weak GDP have been partly pushed by the Atlanta Fed’s GDP updates, that are utilized by the Federal Reserve. Whereas this knowledge raises considerations, it ought to be thought of alongside different financial indicators for a clearer image. It primarily attributes the drop to the commerce steadiness deficit and in the event you dig into the info the imports are skewing these numbers. If we expect for a second why that’s, it doesn’t make a lot sense to base an opinion on that knowledge.

The -2.6% GDP determine raises questions on its accuracy and the components contributing to this drop. Additional evaluation is required to grasp its implications totally.

Supply: Atlanta Fed

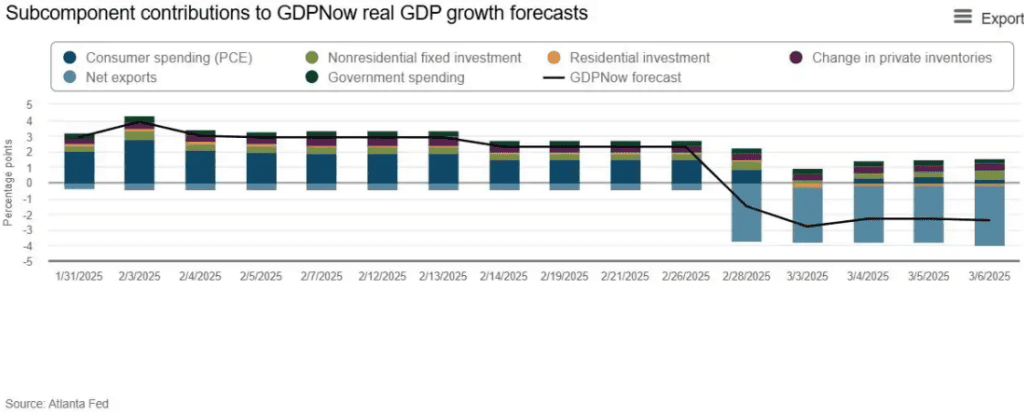

Considerations over tariffs are affecting firms in sure sectors, prompting them to regulate their methods to take care of margins amid uncertainty. Affected firms ship items in bulk earlier than tariffs are imposed. We noticed this being an enormous subject throughout Covid, exacerbated by transport constraints. It acquired so dangerous in Covid that stock ranges acquired somewhat spicy, which precipitated additional points when demand slowed down. Enormous shipments of Gold shifting again to the US is a big a part of this too, it’s not simply shopper items inflicting the numbers to be so off-kilter.

Web exports from the ultimate February print are manner out of character. Displaying big imports offsetting exports.

Vital observe: There’s clearly a decline in exercise because the finish of February 2025, particularly regarding the patron, however not as alarming because the preliminary chart signifies and enhancing after a drop.

Supply: Atlanta Fed

Why is the underside shut, or not less than a bounce?

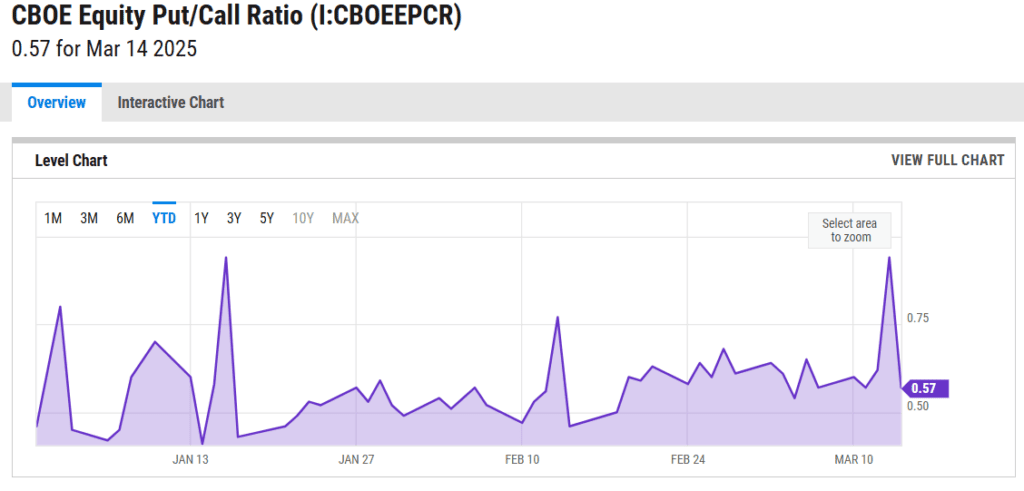

The Fairness Put/Name ratio is again in beneficial steadiness.

Supply: CBOE Fairness Put/Name Ratio Market Each day Insights: CBOE Each day Market Statistics | YCharts

The VIX has cooled off. I’d be happier to see it settle below 20 the decline right here is constructive to see. If this dangerous boy begins rising… We’ll be getting extra draw back.

Supply: My TA

Hedge funds have been unwinding positions in single shares on the quickest fee we’ve got seen in over 2 years, decreasing their market publicity, however nonetheless sustaining a constructive outlook. Suggesting they’re simply rolling with the short-term noise, which is pretty commonplace behaviour for hedge funds. So why am I mentioning this as a constructive indicator? The excellent news is that they’ll have loads of money to deploy once they sit match. It’s this type of danger on investing that drives the V formed recoveries that we frequently see after a correction.

Quantity can also be falling for the SPY, suggesting some vendor exhaustion and the RSI has been at ranges usually solely hit when there’s a robust bounce or reversal.

Supply: My TA

I did wish to briefly contact on some basic market developments. I’m positive you’ve seen a great deal of charts like this recently, however they stand true. If we have a look at prior quickest 10% drops out there, on common 3 months from the drop we’ve got a return of 8.2%, 6 months is a 15% return, and one full yr is a tidy 19.9% return. This occurs no matter a recession or extra draw back value motion.

One factor we do know for positive, is these drops present glorious long-term potential for patrons that may deal with the volatility.

Why I’m shopping for the dip

Most individuals are solely taking a look at this drop with a really short-term view. Does that make sense? No. Treasury Secretary Scott Bessent has been very clear on permitting markets to endure some short-term ache for long run achieve. From a Macro perspective, there’s nice advantages in permitting issues to say no over the brief time period and my expectation is that that is being performed for a number of causes. First, to nudge the Fed into reducing extra aggressively and permitting the US debt to be refinanced at decrease charges. Second, Bessent has additionally been very clear on his need to type out the 10yr and get that fee decrease. A excessive yield places strain on the housing sector, which is a troubled sector proper now. One thing not many individuals point out is that when the yield is low, it could enhance inventory costs as a result of the current worth of future earnings is larger. A better yield can result in decrease inventory valuations as the price of capital will increase, making equities much less engaging in comparison with the risk-free return on authorities bonds.

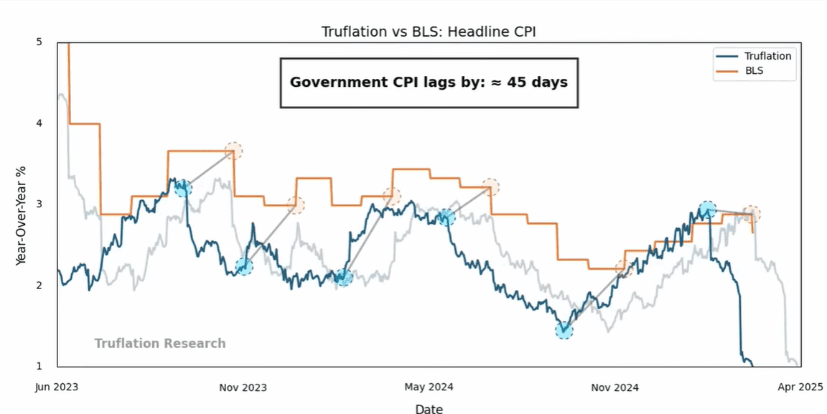

Simply to be clear, I don’t see inflationary dangers to the market. The Fed’s knowledge is considerably lagging (Approx. 45 days behind the Truflation knowledge) so I wouldn’t get hopes up for a right away lower.

Supply: Truflation US Inflation Index | Truflation

Dangers

Quick time period: A hawkish Fed this week that continues with QT may push us decrease and Trumps tariff replace on April 2nd may stoke up worry.

Long run: The ”mortgage disaster” and locked up actual property sector must be addressed, and US debt must be managed, which is what Bessent is ready on coping with.

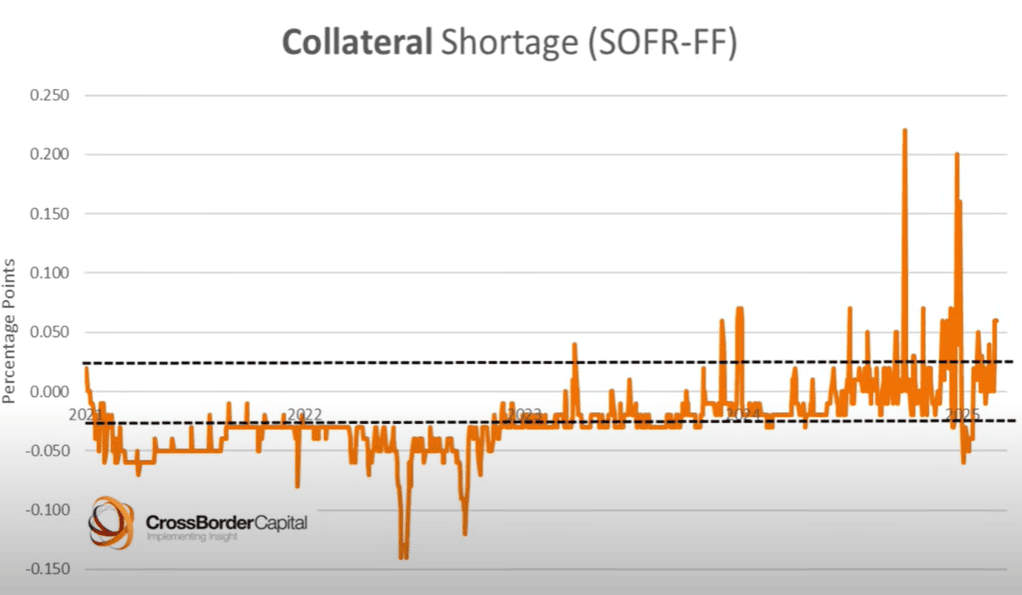

Quantitative tightening is seen liquidity depart the system and it’s trying worrying to me proper now. Most likely the measure I’m most involved with. The M2 measure has acquired folks excited however liquidity is extra complicated than that. US cash markets ought to be sounding some alarm bells to the Fed and it’s actually the guts of the economic system. The SOFR (Repo fee) much less Fed funds unfold has been spiking since July 2024, value ought to be steady throughout the tram strains as they point out the traditional vary. What does this imply? Basically there received’t be sufficient liquidity to maintain establishments that rely upon it, akin to banks, that are seeing falling reserves. Financial institution reserves peaked at $4.2 trillion however have since misplaced over a trillion {dollars}, falling to $3.25 trillion. It’s steered {that a} drop beneath $3.2 trillion, which is simply $50 billion beneath present ranges, may set off a black swan occasion.

Supply: CrossBorderCapital

There are different components which have exacerbated this although, akin to reverse repo’s working dry and all these brief time period issuances Janet Yellen left as somewhat present for Bessent falling off too (It’s possible this was an try to spice up Biden’s re-election possibilities), however that’s stepping into complicated territory and a dialogue about hidden QE/QT. Silver lining although, QE beginning ought to alleviate this strain and in the event that they set the steadiness sheet dimension relative to the debt burden as a substitute of sticking to their present shrinking plan, we may have one much less factor to fret about. It’s attainable that we may see a restoration quickly. One potential answer to alleviate a number of the present pressures may very well be a revaluation of gold, because it hasn’t been adjusted since 1973. This could give the treasury an enormous windfall, assist yields to maneuver decrease so US debt will be refinanced and to allow them to get right down to stimulating.

Conclusion

Whereas there should still be some draw back dangers, it’s attainable that a lot of the market’s current challenges have already been priced in, and my technique doesn’t give attention to timing the tops or bottoms completely. What I love to do, is catch the meat of a transfer, whether or not it’s particular person shares or indexes. I do know it’s very cliché advising folks to purchase when there’s worry and promote when there’s euphoria, however the actuality is, it’s laborious to not fall into the psychological entice and promote on the lows.

One factor I can say with accuracy is, sentiment strikes the market extra simply and quicker than many actual market contagions, each to the draw back and upside. This does give us a number of volatility, however that may additionally give us a number of alternative and that’s what I see right here. Alternative to purchase extra of my favorite shares with some very beneficiant reductions. Will I’ve the prospect to purchase even cheaper? Perhaps, however I don’t wish to fear about timing after I’ll do effectively, given sufficient time, shopping for shares I like over the following 5 years at in the present day’s costs with a 25% to 50%+ low cost.

This communication is for data and training functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out making an allowance for any specific recipient’s funding targets or monetary scenario, and has not been ready in accordance with the authorized and regulatory necessities to advertise unbiased analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product usually are not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}