As soon as a logo of luxurious skincare, Estée Lauder ($EL) is now dealing with challenges, with a lower in gross sales principally due to its Asia gross sales efficiency, with rising competitors from newer manufacturers that resonate extra with youthful shoppers, and in addition new Korean advertising and marketing laws. On Tuesday, February 4th they offered quarterly outcomes, and now the corporate is buying and selling at its lowest valuation in 5 years, let’s analyze their newest numbers.

Key Highlights

Buying and selling at 5 12 months low, is it a discount, or a price lure?

Assessing Estée Lauder’s model and pricing energy in a extremely aggressive skincare market.

Firing 7000 individuals: the corporate’s restoration plan.

Enterprise Mannequin Overview

Estée Lauder is a steward of luxurious status manufacturers, from skincare to haircare, fragrances, and make-up, with a variety of goal clients, and with presence in additional than 150 nations. Based in 1946 by Esther Lauder, with only a number of lotions and perfumes, it’s at this time an organization with greater than 20 manufacturers which have traditionally maintained sturdy model and pricing energy.

Their shoppers have been loyal for years, notably amongst older shoppers. Within the present world, youthful generations are uncovered to skincare from an early age, typically preferring cheaper merchandise. Regardless that The Peculiar, certainly one of their manufacturers, gives higher offers, luxurious manufacturers like Estee Lauder, LaMer, Clinique, and MAC are the true money generator with over 1B in gross sales every.

One notable shift is that 9 Estée Lauder manufacturers have a presence in Amazon US at this time when beforehand they didn’t promote on Amazon in any respect. Among the manufacturers are underneath the “Premium magnificence” class, signalling a strategic transfer to adapt to digital shopper behaviour. One other instance is that they now have a presence in TikTok store UK. Regardless of this, the corporate faces mounting pressures from opponents that dominate on-line gross sales and influencer partnerships, and with the brand new pattern on Korean Magnificence, Dr.Jart+ one of many Korean magnificence manufacturers of Estee Lauder, now has extra competitors than ever as a result of the US market is the largest shopper in skincare worldwide. If shopper preferences change in direction of Korean magnificence manufacturers, all the opposite manufacturers of the corporate must adapt reasonably shortly.

Funding Thesis

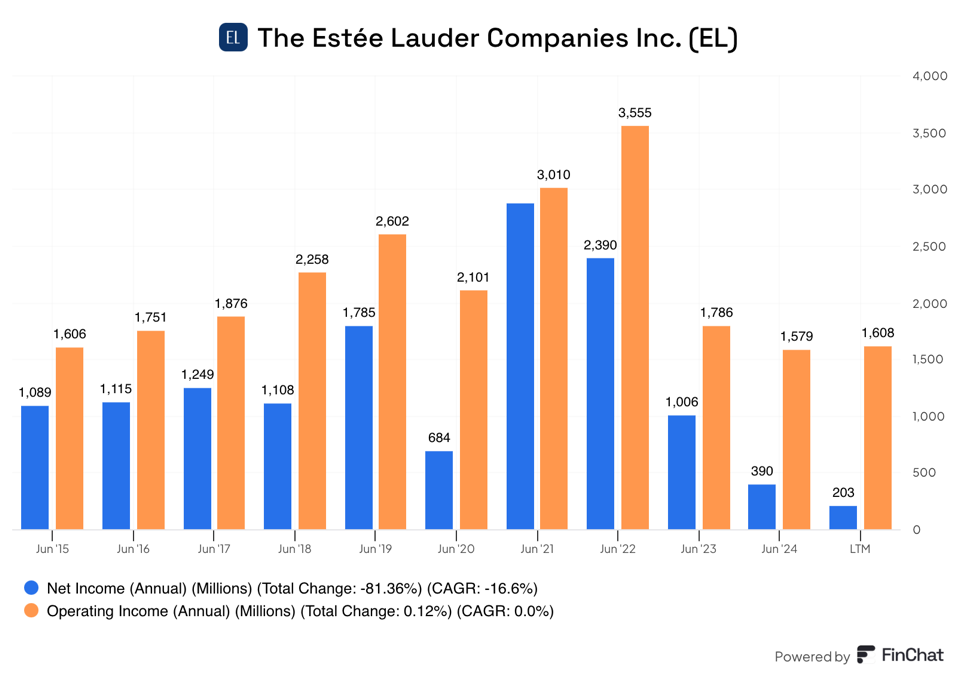

Whereas Estée Lauder has lengthy been a powerful participant within the luxurious magnificence business, latest monetary struggles elevate considerations. The corporate’s newest annual report, and the latest second quarterly outcomes, point out a difficult retail setting, with declining gross sales in key markets. For instance, Asia with a -11% in gross sales in the course of the earlier six months. Additionally, web gross sales decreased in whole -6% newest quarter to $4 billion. And the steerage for the third quarter is just not optimistic in any respect. This has damage the working margin, which is now the bottom of the last decade.

Supply: Finchat.io

To face this problem, Estée Lauder has launched the Revenue Restoration and Development Plan (PRGP), referred to as “Magnificence Reimagined” which goals to enhance value efficiencies and drive sustainable progress with an estimated reaching date for 2027.

Due to this turnaround try, the corporate expects one other income discount within the subsequent quarter. As a part of this PRGP, they count on to spend between 1.2 billion and 1.6 billion earlier than taxes on employee-related prices (between 5.800 and seven.000 job cuts from 62.000 workers).

The massive query right here is, can $EL keep the earlier working margin whereas sustaining or rising revenues, or are they a part of the previous now?

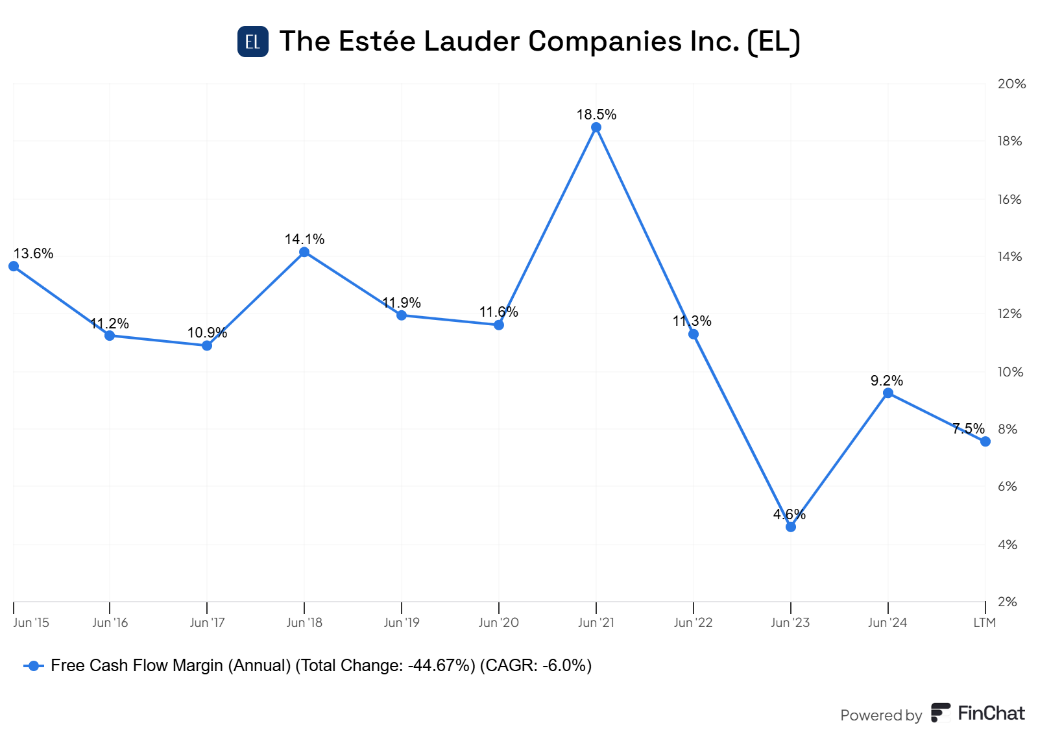

Though we all know that subsequent 12 months goes to be difficult when it comes to margins and income, we goal to calculate the corporate’s sustainable free money move. For that purpose, we construct three totally different eventualities. Base, pessimistic, and optimistic.

It is a firm with a stable background and has luxurious manufacturers with pricing energy. Within the pessimistic state of affairs, in case the corporate doesn’t obtain an enchancment in its web margins, the corporate remains to be overvalued. Nonetheless, if they will handle to get again to their regular margins, which they’re making an attempt to realize by means of their PRGP program, the corporate might ship an annual return of over 14% in the course of the coming three years.

Supply: Finchat.io

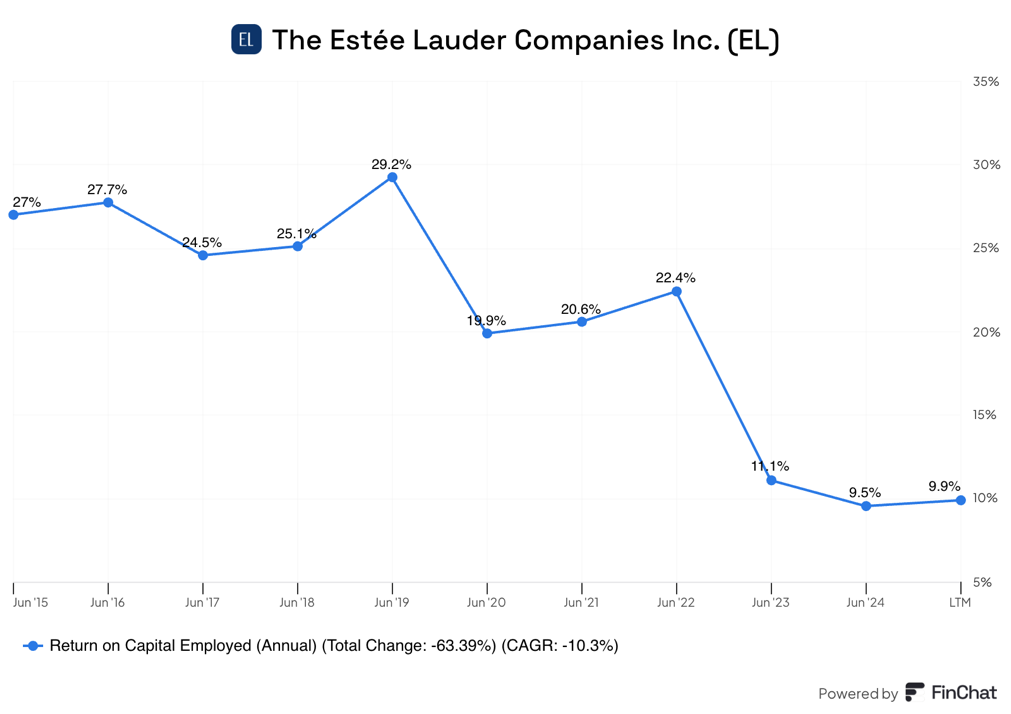

As we are able to discover within the graphic under, the returns on capital employed have been steady since 2015, with a median of 24,55% in eight years. This made the corporate commerce a P/E valuation inside the 30x- 40x vary. So, if the corporate improves its margins, this may improve its present ROIC as properly, and it might result in a greater margin than our optimistic valuation.

Supply: Finchat.io

Dangers

Declining model energy: Regardless of their lengthy trajectory within the sector, new know-how and discoveries in skincare and new globalized skincare traits, shifts in Korean magnificence, and influencers-led manufacturers are a real concern for the model.

New leaders: Stéphane de la Faverie, took place in January 2025 and he has a observe file of being normal supervisor for some corporations within the magnificence sector. Nonetheless, that is his first time being a CEO, and he’s in a extremely unhealthy place to start out studying. Different members of the crew, just like the CFO are retiring, which could possibly be additionally a possibility for brand new and extra up to date concepts to the brand new technology’s wants.

Execution of their PRGP: Turnarounds have confirmed to be tough to implement, and as traders we now have to firmly imagine within the administration functionality to implement well timed measures to vary the trail of the corporate.

Macroeconomic threat: we noticed within the pandemic interval of 2020, a big discount of their gross sales, and it is a show that $EL can be affected by the financial setting.

Solvency threat: If the corporate can’t recuperate its margins, and revenues hold deteriorating, the debt that the corporate holds can grow to be a significant downside. With 6 billion in web debt, they’ve the danger of being unable to pay their obligations.

Regulatory challenges: They acknowledge one of many main impacts on the gross sales was the Korean guideline for e-commerce, being Korea roughly 10% of their gross sales. It’s identified that advertising and marketing methods play with the urgency and requirements of the buyer. Listed below are among the new pointers:

The way in which that they promote their costs and product dimension.

Restrictions within the subscription program.

Collaborations with influencers, they now must disclose within the title or to start with of the advice that they’re being paid to say that.

This makes a big impression on advertising and marketing methods, which want now a very totally different restructuring to adjust to the Korean regulation.

Rivals

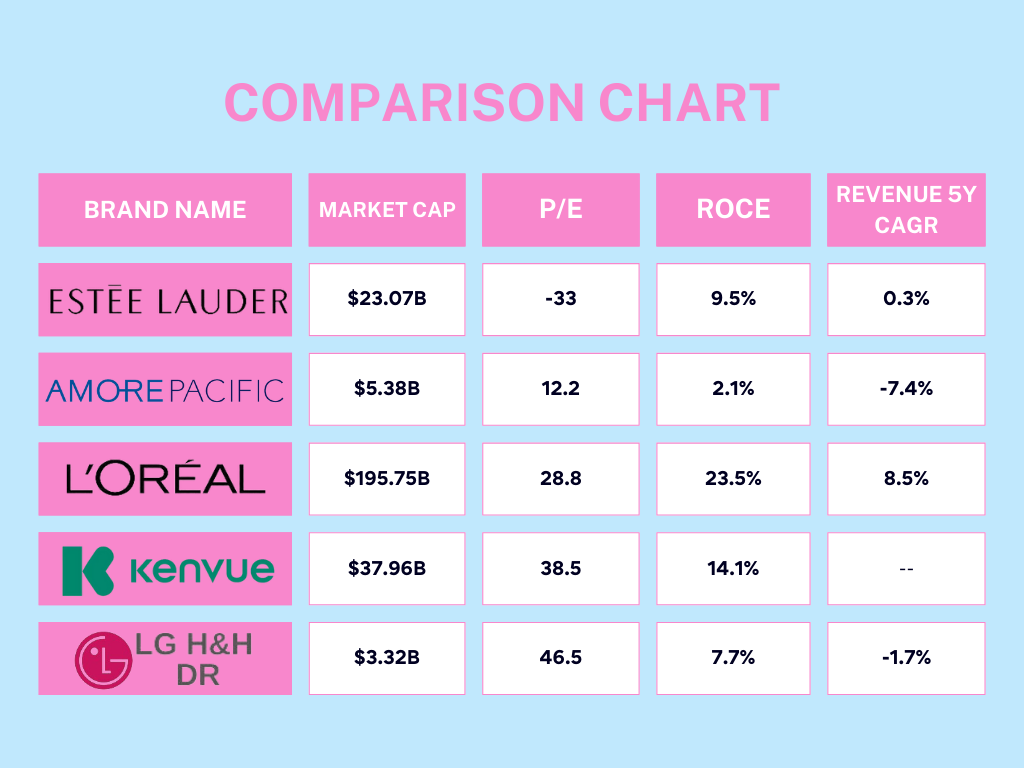

Loreal: The most important competitor with a market cap of 192.37 Billions.

Korean magnificence manufacturers: as LG H&H, and Amorepacific corp, Goodai.

Conclusion

The Revenue Restoration and Development Plan (PRGP) is a stable technique to deal with Estée Lauder’s challenges, however with a two-year timeline for execution, remains to be within the early stage of execution. My place stays cautious so, I desire to attend for the following quarter’s outcomes to evaluate whether or not significant enhancements in value administration and operational effectivity are taking form. Whereas the corporate possesses sturdy manufacturers, administration should reveal a transparent dedication to driving a profitable turnaround.

One promising growth is the mixing of AI into operational processes, enhancing effectivity in stock forecasting and materials planning. Early outcomes counsel improved margins, signaling a willingness to embrace technological developments and adapt to a brand new period of shopper habits.

Nonetheless, there’s a threat that Estée Lauder might grow to be a price lure, a inventory that seems low cost however continues to say no resulting from structural weaknesses, with out a confirmed observe file of the brand new administration it is a risk. Whereas the corporate’s model fairness stays sturdy, the rise of recent opponents, shifting shopper preferences, and execution dangers in its restoration plan might restrict long-term upside.

At present ranges, I’m not investing in Estée Lauder, but when the inventory reaches a extra engaging value that provides a prudent margin of security, it might grow to be a compelling alternative. For now, my advice is to maintain $EL in your watchlist and monitor whether or not administration can execute its turnaround successfully. On this case, though the value can doubtlessly go up, we’d have extra certainty concerning the firm’s valuation, so the danger would diminish.

What do you suppose? Is Estée Lauder on the trail to restoration, or is it a basic worth lure?

{kind=link}